This article provides comprehensive information regarding BHA Services, a debt collection agency, and its practices. It aims to inform consumers about potential issues with debt collection, differentiate between legitimate agencies and scammers, and outline steps for protection and recourse.

BHA Services: A Debt Collection Agency

BHA Services operates as a debt collection agency. Their primary function is to purchase past-due debts from original creditors and then attempt to collect these outstanding amounts from consumers. While BHA Services is a legitimate entity in the debt collection industry, the sector itself is known for deceptive practices.

Key points to consider when dealing with BHA Services:

- BHA Services may employ aggressive tactics during their collection attempts.

- Legally, they are required to provide consumers with detailed information about any debt they are attempting to collect.

- Consumers often report feeling pressured by debt collectors to pay immediately, which can be a significant red flag.

It is crucial for consumers to understand their rights when interacting with debt collectors. If you suspect you are dealing with a scam or find the practices of a collection agency questionable, seeking assistance from consumer protection agencies is recommended.

The Role of BHA Services in Debt Collection

BHA Services collects debts on behalf of various creditors, commonly including payday loan companies and other types of lenders. However, the specific identities of these original creditors are not always disclosed, a common occurrence within the debt collection industry.

When BHA Services appears on your credit report, it typically signifies an outstanding debt that they have acquired. Such listings can negatively impact your credit score. To gain a comprehensive understanding of any debts affecting your score, it is advisable to obtain your 3-bureau credit report. Knowing which creditor BHA Services is collecting for can assist you in effectively managing your financial situation.

Why BHA Services Appears on Your Credit Report

Your credit report may list BHA Services because they have purchased a debt you owe from an original creditor for which you ceased making payments. This situation commonly arises when bills go unpaid, prompting the original creditor to sell the debt to a collection agency like BHA Services. They then endeavor to collect the owed amount, and reporting the debt on your credit report is one of their collection tactics.

It is essential to verify the legitimacy of any debt reported by BHA Services. If you do not recognize the debt or believe it is inaccurately reported, it is crucial not to contact BHA Services immediately. Instead, take the time to review your records and confirm the validity of the debt, as you are not necessarily obligated to pay if the information on your credit report is incorrect. Remember, if they fail to report accurate information to the credit bureaus, they are required to remove the entry from your report.

In summary, BHA Services typically appears on your credit report as a consequence of unpaid debts you have incurred. It is vital to double-check the legitimacy and accuracy of the reported debt before taking any further action.

Scams vs. Legitimate Debt Collection

The Better Business Bureau (BBB) has noted a significant number of complaints related to both debt collection scammers and legitimate debt collection companies. Consumers have reported receiving harassing phone calls and texts from individuals claiming to be from entities like BHA Services, demanding payment for debts they do not owe.

Fake Debt Collectors and Scammers

Scammers often impersonate legitimate debt collectors or payday loan companies. They may use stolen financial information to pressure consumers into paying. These schemers frequently utilize difficult-to-trace payment methods such as gift cards, payment apps, and money orders. Their tactics often involve instilling fear, with threats of legal action or jail time if payment is not made promptly.

Between 2019 and 2021, the BBB's Scam Tracker received over 7,800 reports concerning loan and debt collection scams, resulting in reported losses of $4.1 million. Melanie Duquesnel, president and CEO of the local Better Business Bureau, advises consumers to hang up if they receive calls demanding payment for a debt they do not believe they owe.

Legal Businesses with High Complaint Volumes

Beyond outright scams, many legitimate businesses in the short-term loan and debt collection sector also receive a high volume of consumer complaints. A BBB study revealed that many payday loan companies:

- Offer interest rates calculated on a weekly or bi-weekly basis, rather than annually.

- Target individuals in urgent need of cash who may struggle to repay the loan quickly.

- Trap borrowers with accumulating fees, triple-digit annual interest rates, and short repayment schedules.

From 2019 to 2021, the BBB recorded over 117,000 complaints against legal loan and debt collection companies, with more than $118 million in disputed amounts.

Protecting Yourself from Debt Collection Issues

Consumers can take several steps to protect themselves from deceptive debt collection practices and predatory lending:

For Short-Term Loans:

- Read the Fine Print: Carefully review all terms and conditions before signing any paperwork for a short-term loan. Ensure you fully understand the interest rate and all associated fees.

When Contacted About Debt:

- Verify the Debt: If someone calls claiming you are overdue on a debt that is several years old (e.g., 10-15 years), it is often advisable to simply hang up. If you are unsure about the amount you owe, contact your creditors directly to verify the details.

- Never Pay with Risky Methods: Avoid paying debts through payment apps like Venmo or with gift cards. Legitimate creditors will accept traditional payment methods, including checks.

Reporting Concerns:

If you believe you are a victim of a scam, or if a loan company appears to be hiding excessive interest rates, report your concerns. You can register complaints with the following entities:

- Better Business Bureau Scam Tracker

- Federal Trade Commission (FTC)

- Michigan State Attorney General

For overdue payments on payday loans, the BBB suggests exploring resources from the Consumer Financial Protection Bureau (CFPB). These resources can help you understand debt collection processes and your rights. Additionally, consider setting up a payment plan or working with debt counselors from non-profit organizations like Greenpath Financial Wellness.

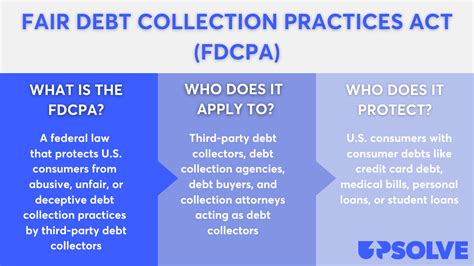

Understanding Your Rights and Debt Validation

The Fair Debt Collection Practices Act (FDCPA) provides consumers with specific rights when dealing with debt collectors. One crucial right is the ability to request debt validation.

Requesting Debt Validation:

If BHA Services contacts you about a debt, you have the right to request a debt validation letter. This letter must include specific details about the debt, such as the amount owed and the original creditor's information. According to the FDCPA, BHA Services is required to provide this information within five days of their initial contact with you.

If you have not received this letter, you should request it directly by calling BHA Services or sending a written request. You have 30 days from receiving the validation information to dispute the debt if you believe it is inaccurate. Ensure your dispute is submitted in writing, as this places a hold on collection efforts while BHA Services responds to your request.

Disputing Inaccurate Debts:

When writing your dispute, clearly state your reasons. For instance, you might state, "I do not owe this debt," and request proof that validates its legitimacy. If you are uncertain about how to proceed, seeking assistance from a credit repair company can help guide you through the process and ensure your rights are protected.

To dispute and potentially remove an inaccurate BHA Services entry from your credit report, begin by obtaining your credit reports from the three major bureaus: TransUnion, Equifax, and Experian. Carefully review each report for any errors related to BHA Services. If inaccuracies are found, gather supporting documents (e.g., payment receipts, account statements) and send a verification letter to BHA Services requesting proof of the debt. Working with a reputable credit repair company can assist in drafting dispute letters tailored to your situation.

Impact of BHA Services on Your Credit Score

Having BHA Services listed on your credit report can significantly harm your credit score. When a debt collector reports an unpaid debt to credit bureaus, it negatively affects your payment history, a critical component of your credit score. This can lead to a substantial drop in your score, especially for larger debts.

Collection accounts typically appear on credit reports after approximately 180 days of non-payment and can remain for up to seven years from the original delinquency date. This prolonged presence can hinder your ability to secure future credit.

Consequences of Collections on Credit Reports

- Credit Score Reduction: Collection accounts can lower your credit score, particularly if they stem from missed payments.

- Lender Perception: Lenders may view a collection account as a red flag, perceiving you as a higher risk and potentially leading to loan rejections or higher interest rates.

- Credit Utilization Ratio: Unpaid debts reported by collectors can negatively affect your overall credit utilization ratio, further diminishing your credit score and borrowing power.

To mitigate the impact, it is essential to address any overdue accounts promptly. Communicate with BHA Services regarding repayment options or disputes if you believe there are inaccuracies. Proactive measures are crucial for maintaining a healthy credit profile.

To Pay or Not to Pay: The "Pay for Delete" Option

Paying off a debt listed by BHA Services will not automatically remove it from your credit report. Even after settling the amount, the collection account can remain on your report for up to seven years from the original delinquency date, as mandated by the Fair Credit Reporting Act.

Payment updates the balance to zero but does not erase the historical negative entry. While a "pay for delete" agreementâwhere you pay a portion or the full amount in exchange for the removal of the collection accountâcan be beneficial, especially for smaller debts (generally under $100), it's not universally supported by credit reporting agencies. Any such agreement must be obtained in writing before payment is made.

Negotiating a "pay for delete" with BHA Services requires a formal offer, either by phone or a written letter. Be aware that many collectors may be reluctant to agree to this arrangement. If they do agree, ensure you have signed confirmation. Without it, they might accept payment without removing the account.

Alternatively, settling a debt with BHA Services may not be the best strategy. A settled debt can still appear as a negative item on your credit report for up to seven years, potentially hindering future credit applications. Settling might even be more damaging than ignoring the debt if you lack a solid plan for managing your financial obligations.

Before engaging in settlement or payment, focus on verifying the debt's legitimacy. If the debt is under $100, consider settlement after understanding its implications on your credit report. Consulting a financial advisor or credit counselor is wise to map out a sustainable repayment strategy.

Stopping Harassment from BHA Services

If you wish to stop BHA Services from contacting you, several strategies can be employed:

- Block Numbers: Block their numbers directly through your phone's settings or use a call-blocking application.

- National Do Not Call Registry: Register your number with the National Do Not Call Registry to reduce telemarketing calls, though this may not completely prevent BHA Services from contacting you.

- Ignore Calls (Cautiously): While ignoring calls might reduce immediate annoyance, it does not resolve any outstanding debts.

- Cease Communication Request: Send a formal written request asking them to cease communication. A legitimate agency is legally obligated to respect this request and halt further contact.

- Seek Professional Assistance: Consider reaching out to a reputable credit repair company for assistance. They can help analyze your credit report and develop a plan to stop unwanted contact from BHA Services.

It is important to note that ignoring BHA Services is not a viable long-term solution. Unaddressed debt can lead to negative credit reporting, increased aggressiveness from collectors, and potential legal action, including wage garnishment.

Contact Information for BHA Services

BHA Services can be contacted at the phone number 855-203-6663. No identifiable physical address was found. Be aware that debt collectors like BHA Services may use various local numbers to try and entice you to answer their calls.

It is highly recommended to avoid reaching out to them directly without proper preparation. Instead, consider pulling your three-bureau credit report for a comprehensive analysis of your credit situation to ensure you are well-informed about any outstanding debts before engaging with the collection agency.